Powerful Personal Finance Strategies

Learn powerful personal finance strategies to take control of your money, from budgeting and debt management to investing and setting financial goals. Discover actionable tips that can help you achieve long-term financial security and peace of mind.

No time to read? Listen to the Podcast.

Contents:

Introduction: Taking Control of Your Personal Finances – A Journey Toward Financial Freedom and Security

After my daughter Shrivi’s first birthday, I stood at a crossroads in my life. The desire to take financial control of my future perplexed me, a feeling most of you can relate to. I was unsure of which way to go. The many investment options and technical jargon surrounding it left me paralyzed. I was afraid of making any wrong move and losing my hard-earned money. But the thought of securing my daughter’s financial future hardened my resolve. So, I began to learn some really simple personal finance strategies.

As my learning journey began, the fog surrounding finance and investments cleared. I discovered the importance of understanding financial and investment opportunities, which allows individuals to make informed financial decisions that align with their goals and constraints. As I learned more, I saw that finance and investing are for everyone. It’s empowering to gain that experience. This article aims to guide you to financial freedom. It will simplify the process for a college student, a business leader, a homemaker, or a freelancer. I will share my experiences to help you navigate your finances. It will give you clear, actionable steps to do it with confidence. This knowledge will empower you, just as it has empowered me. Let’s begin our journey to financial freedom.

Why are Personal Finance and Financial Planning Crucial for Achieving Your Financial Goals?

The financial planning process is important and goes beyond just managing money. It ensures your finances support your life goals and values. Financial planning lets you make informed decisions and aligns your actions with your interests. It covers budgeting, saving, investing, and retirement planning, each playing a big role in your financial future. You can grow and be financially stable by understanding and applying these concepts. You and your loved ones will be ready for whatever life throws at you.

Personal Financial Management: Essential Strategies for Everyone

Income: Your income is the basis of your financial plan. It comes from your salary, business income, savings interest, or rental income. You must have a bank account to manage your income. It helps you track your earnings, monitor expenses, and avoid overspending and debt.

Expenses: It’s vital to manage regular costs like rent, groceries, education, and entertainment to stay financially balanced. Effective personal finance management requires knowing where your money goes each month. It helps you live within your means and avoid debt.

Savings: Saving for future needs is important for financial security. This includes emergencies, children’s education, and a wedding. A dedicated savings account helps you save. It also provides a safety net for life’s expected and unexpected events.

Investments: They encompass a variety of assets, including mutual funds, stocks, bonds, real estate, and gold. Each asset class carries its own risk and return profile. For instance, stocks tend to offer higher returns but come with increased volatility, while bonds provide more stability but with lower returns. Diversifying your investments across these asset classes can help manage risk while maximizing returns. Consider strategies like cost averaging, where you invest a fixed amount regularly to reduce the impact of market volatility, and rebalancing your portfolio periodically to maintain your desired asset allocation.

Debt: Debt includes any money you owe, like home loans, education loans, or credit card balances. Managing debt is important to maintain financial health. It means paying on time, knowing the cost of borrowing, and avoiding too much debt that can hurt your financial progress.

By covering these areas with personal financial planning, you can take control of your financial future. It will reduce stress and give you a roadmap to achieve your life goals.

The Importance of Budgeting in Personal Finance and Effective Cash Flow Management

Budgeting is the basis of personal finance. In India, saving for the future and family is a big cultural value. A budget is more than a tool; it’s a roadmap. It helps you track your expenses, plan for big expenses, and save for long-term goals. It’s the key to personal finance and personal finance management.

How to Create a Personal Budget for Managing Expenses and Achieving Financial Stability?

List your income: Include all sources, such as salary, freelance work, interest, etc.

List your expenses: Divide them into essentials (rent, groceries) and non-essentials (dining out, subscriptions).

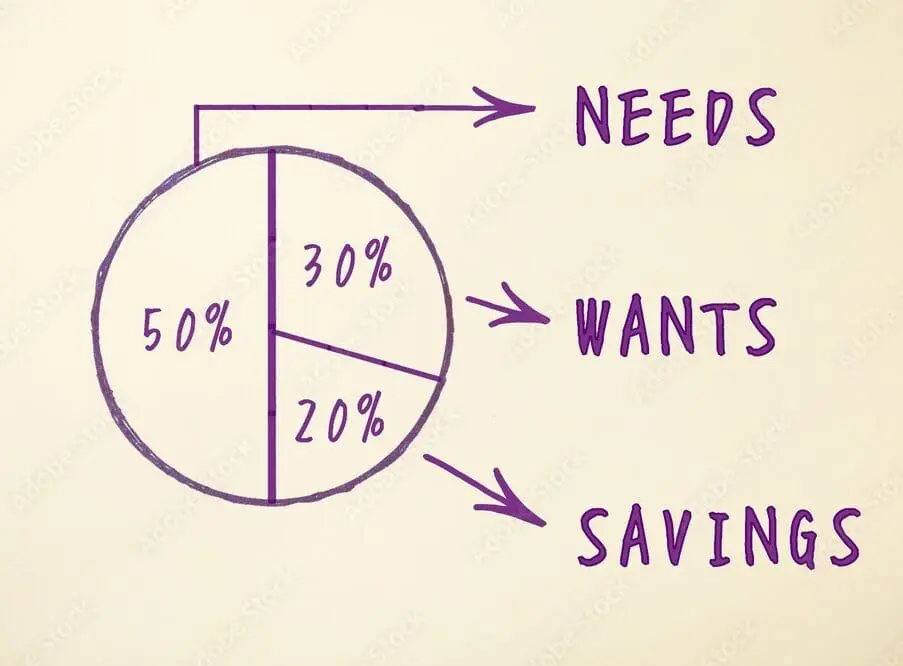

Balance the Two: Implement the 50/30/20 rule for budgeting, where 50% of your income is allocated to essentials (like rent and groceries), 30% to discretionary spending (like entertainment), and 20% to savings and investments. For a more detailed approach, consider zero-based budgeting, where every rupee is assigned a purpose, ensuring no money is left unaccounted for. Use tools like our downloadable budgeting template to categorize your expenses and set realistic spending limits.

For example, if you earn ₹50,000 a month, you might allocate:

₹20,000 for rent and utilities,

₹5,000 for groceries,

₹15,000 for entertainment,

₹10,000 for savings and investments.

This simple budget helps you save for the future while meeting your needs now.

Personal Finance Apps for Budgeting and Expense Tracking

Personal finance apps can transform how you manage your money and play a crucial role in personal finance management. They make budgeting easier and more effective. Apps like Moneydance and Walnut help you track spending, categorize expenses, and set financial goals. These apps sync with your bank accounts and credit cards. They update you in real-time on your spending habits. This helps you see where your money is going and makes it easier to stick to your personal budget.

Also, personal finance apps do more than track expenses. They are part of your overall financial planning. These apps can help you show your spending habits and find where to cut back. You can also set goals and track your progress. These apps will help you align your finances with your long-term goals and save for a big purchase, plan for retirement, or manage daily expenses.

Managing Personal Finances: Tracking and Cutting Unnecessary Expenses

Money management starts with knowing where your money is going. Tracking your expenses. Cutting any unnecessary ones. And making informed decisions to improve your financial health.

Tools to Track Expenses

When choosing a personal finance app, selecting one that best fits your needs is important. For example, Moneydance offers comprehensive budgeting tools and investment tracking, making it ideal for those with diverse financial needs. On the other hand, Walnut is excellent for expense tracking and budget management, offering a simpler interface for users who want to focus primarily on day-to-day expenses. For those interested in enhancing their financial literacy, online courses such as Zerodha Varsity provide in-depth knowledge on investing. In contrast, NISM certification courses can equip you with professional-level expertise in specific financial domains.

Cutting Expenses

Once you have a clear view of your spending habits, the next step is to cut back on unnecessary expenses. Small changes in your spending can add up to big savings over time. For example, if you see you are spending ₹2,000 a month on dining out, cut that down to ₹1,000. This would save you ₹12,000 a year. You could then use it for savings, investments, or debt repayment.

These small changes may seem minor. But they can add up to help you build a more secure financial future. You can reinvest these savings in what matters most to you. You could fund a retirement, an emergency, or a vacation fund. Then, your money will work toward your long-term goals.

Tracking your expenses with personal finance apps lets you take charge of your money. It can reduce stress and help you succeed financially in the future.

Emergency Funds: The Backbone of Personal Finances and Financial Security Against Unexpected Events

An emergency fund is an essential part of any personal finance strategy. Often called the backbone of financial planning, it is a safety net. It helps you manage unexpected expenses while maintaining your long-term goals. It protects you from financial shocks and helps with unexpected medical emergencies leading to medical expenses, job losses, or car repairs. With it, you can avoid debt and not sell your investments.

In India, families value financial security, making it crucial to have a fund that covers your essential expenses in tough times. It lets you focus on solving the crisis rather than on money. It’s recommended to save 3 to 6 months of your living expenses. This range gives you flexibility, depending on your situation. Those with stable jobs can go for the lower end. Those in volatile industries can go for the higher end.

If your monthly expenses, including rent and groceries, are ₹30,000, your emergency fund should be ₹90,000 to ₹1,80,000. This fund is not just about having money in the bank; it’s about peace of mind. A financial cushion can ease financial stresses in tough times and provide immediate personal protection in uncertain times.

Steps to Build an Emergency Fund:

Calculate Your Monthly Expenses: First, calculate your essential monthly costs. These include housing, utilities, groceries, transport, insurance, and any debt payments. This will give you a clear picture of how much you need to save.

Set a Savings Goal: Set a target for your emergency fund based on your monthly expenses. For example, if your expenses are ₹30,000 per month, your goal should be to save between ₹90,000 and ₹1,80,000. Adjust this amount based on your situation. Consider job stability, health, and family duties.

Automate Your Savings: To reach your goal, automate your savings to ensure progress. Set up a recurring transfer from your primary bank account to a dedicated emergency fund account. Even small, regular savings can add up and make a big difference over time.

Keep Your Fund Accessible but Safe: Your emergency fund should be easy to access in an emergency. But it shouldn’t be so easy that you are tempted to use it for non-emergencies. A high-yield savings account or a liquid mutual fund can be good. They offer liquidity and some growth on your savings.

Replenish After Use: If you use your emergency fund, replenish it ASAP. Life is unpredictable, and restoring that cushion will prepare you for the next unexpected event.

An emergency fund is key to financial stability and independence. This fund will be your financial lifeline. It will give you the confidence to face life’s uncertainties. It will not risk your family’s finances and ensure your financial independence.

Managing Debt and Credit Scores: Essential for Personal Finance and Financial Health in India

Debt is a reality for many of us, whether it’s education loans, home loans, or credit card debt. Debt in India is associated with the CIBIL score, which financial institutions use to assess creditworthiness. Your CIBIL score is a number from 300 to 900. It reflects your creditworthiness based on your financial history. This score shows how well you have managed loans and credit cards in the past. A higher score means good credit management and can help you get loans or credit cards with better terms. Banks and lenders use this score to decide on your loan or credit application and the interest rate. To keep a good CIBIL score, pay your bills on time. Use credit wisely, and don’t apply for too much credit at once. Managing personal finance, including debt, is crucial for your CIBIL score. It affects your ability to get better-paying loans.

How to Manage Debt and Credit Card Balances Effectively

Managing debt is key to financial health and long-term goals. Here’s how to do it:

Pay On Time: A key debt management rule is to pay your EMIs (Equated Monthly Installments) and credit card bills on time. Timely payments will help you avoid late fees and penalties. They will also protect your CIBIL score, which affects your ability to borrow in the future. Set up automatic payments or reminders so you never miss a due date.

Pay More Than the Minimum: Paying only the minimum payments on credit cards can lead to high interest and a longer repayment period. Try to pay more than the minimum. It will reduce your principal balance faster. It’ll save you on interest and help you become debt-free sooner.

Avoid Unnecessary Debt: Only borrow what you can afford to repay. Before taking on new debt, ask yourself if it’s truly necessary. For example, avoid personal loans for discretionary expenses, like vacations or luxury items. Instead, save up for these expenses to avoid adding to your debt burden.

Good Debt vs. Bad Debt

Not all debt is equal. Knowing the difference between good and bad debt can improve your finances.

Good Debt: Good debt is borrowing, which is an investment in your future. It involves loans that are used to acquire assets that can appreciate in value or generate income over time. A home loan is a good debt. Real estate usually appreciates. Owning a home gives long-term financial security. Similarly, student loans can be considered good debt if they lead to a degree that increases earning potential.

Bad Debt: Bad debt is borrowing that doesn’t contribute to your financial well-being. This includes high-interest debt used to buy non-essential items that don’t appreciate in value. Credit card debt for luxury purchases and discretionary expenses is bad debt. With no financial gain, you pay more for the item due to interest. Bad debt can spiral out of control and make it harder to achieve financial stability.

Manage debt responsibly and use credit cards wisely. Pay on time, pay more than the minimum, and avoid unnecessary debt. Doing so will keep your financial profile healthy. By knowing good and bad debt, you can make better choices. They will help your long-term goals, reduce stress, and secure your future.

Proven Strategies to Improve Your CIBIL Score and Enhance Your Financial Planning

A high CIBIL score opens doors to better loans and credit cards. Consistent effort and disciplined financial habits are required to maintain a healthy CIBIL score. Here’s how you can work on it:

Pay Bills on Time: Timely payments are one of the biggest factors that affect your CIBIL score. Whether it’s EMIs, credit card bills, or utility payments, ensure you never miss a due date. Set up automatic payments or reminders so you pay on time, every time.

Keep Credit Utilization Low: It’s the percent of your available credit that you use. Ideally, using less than 30% of your credit card limit would be best. For example, if your credit card limit is ₹1,00,000, try keeping your outstanding balance below ₹30,000. Lower credit use shows lenders you don’t rely on credit. This can boost your score.

Maintain Older Credit Cards: The length of your credit history information contributes to your CIBIL score. The longer you have a credit card or loan, the more information is available to assess your creditworthiness. Even if you rarely use an old credit card, keep it active. Make some small purchases to maintain a long, positive credit history.

Avoid Frequent Credit Applications: Every time you apply for a new credit card or loan, it results in a hard inquiry on your credit report. Multiple hard inquiries in a short period can negatively affect your CIBIL score. Apply for credit only when necessary and avoid multiple applications at once.

The ABCs of Personal Finance: Smart Savings and Investment Opportunities for a Robust Financial Strategy

In India, saving is in our blood; we have a culture of saving for the future. However, saving is just one part of a larger financial strategy. To grow your wealth and gain financial freedom, combine saving with smart investing. Here’s how to save and invest:

Principles of Saving and Investing

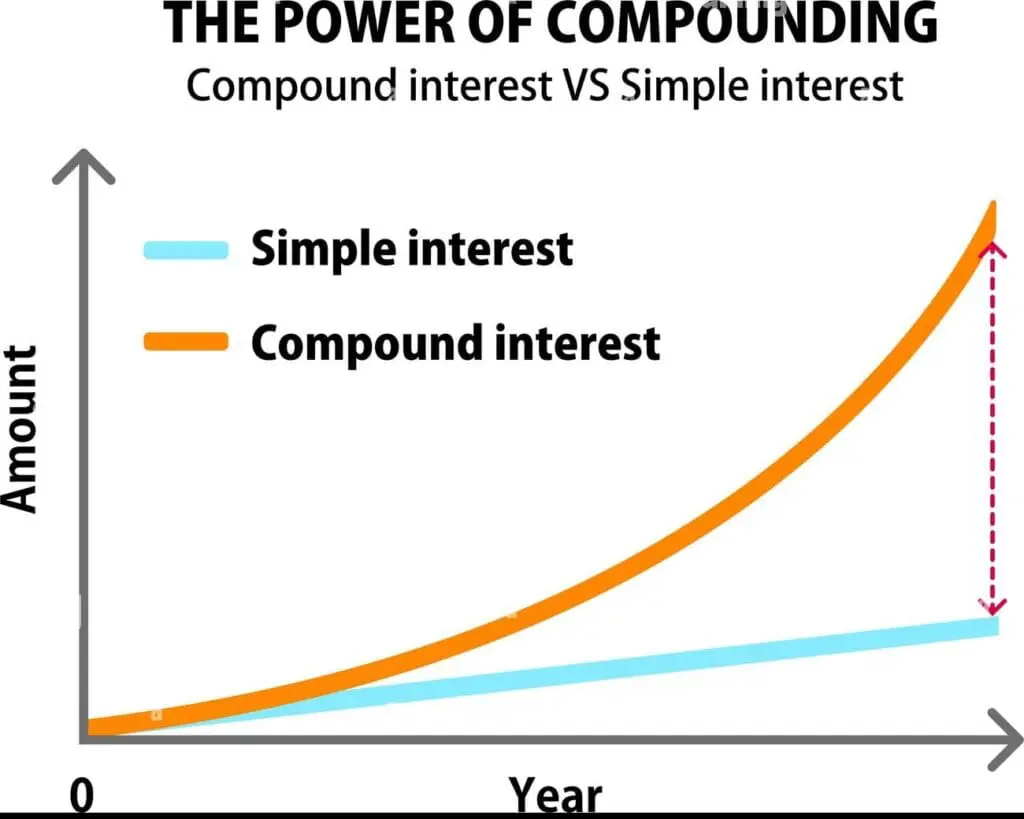

Start Early: The sooner you start saving and investing, the more time your money has to grow. This is because of the power of compound interest, where the interest you earn also starts earning interest over time. Even small amounts saved and invested early can grow big over time, leading to substantial savings.

Leverage Government Schemes: Take advantage of India-specific investment opportunities like the Pradhan Mantri Vaya Vandana Yojana (PMVVY), which offers a guaranteed return for senior citizens, or the Sukanya Samriddhi Yojana (SSY) for your daughter’s education and marriage. These schemes provide tax benefits and secure returns, aligning with long-term financial goals in the Indian context.

Save Regularly: Consistency is key when it comes to saving. Saving part of your monthly salary, or a fixed weekly amount, can build your financial cushion. Making it a habit will ensure you save regularly. Even small amounts add up over time. They can build a strong foundation for future financial security.

Diversify: It means spreading your investments across asset classes. These include stocks, bonds, real estate, and fixed deposits. This reduces risk as one investment’s good performance can offset another’s poor performance. A well-diversified portfolio is less likely to suffer big losses. It helps protect your wealth over time.

Understand Your Risk Tolerance: Every investment has some level of risk. You must know your risk tolerance or the risk you will take. It is key to choosing the right investment strategy. For example, stocks are riskier but offer higher returns. Fixed deposits are safer but offer lower returns. Assess your financial goals, time horizon, and risk tolerance. This will help you find the right investment mix.

These principles will help you manage your finances, build wealth, and achieve your long-term goals. To succeed financially, you need to improve your CIBIL score, save for the future, and invest to grow your wealth. The keys are disciplined habits and informed choices.

Compound Interest: The Magic Potion to Grow Your Wealth Through Smart Financial Planning

Compound interest is the interest earned not just on your principal amount but also on the interest that has already been added to it. The frequency of compounding—whether it’s annually, semi-annually, quarterly, or monthly—can significantly affect your investment’s growth. For example, if you invest ₹10,000 at a 10% annual interest rate compounded annually, you would earn ₹1,000 in the first year. However, if the interest is compounded quarterly, your total interest earned would be slightly higher due to the compounding effect occurring more frequently. Over time, this seemingly small difference can lead to substantial growth in your investment.

A big part of personal finance is compound interest. It’s important for managing and growing your money over time.

Essential Investment Concepts: Elevate Your Personal Finance Education and Discover New Opportunities

Investment can be scary. But knowing some basics can help you navigate the equity markets better. Personal finance courses online can give you the foundation to start investing wisely.

Risk and Return: Higher returns come with higher risk. For example, equities (stocks) offer high returns but are volatile.

Diversification: Spread your investments across different asset classes—stocks, bonds, and real estate. This reduces risk.

Active vs. Passive Investing: Active investing involves frequent buying and selling of assets. Passive investing is about buying and holding assets for the long term.

Portfolio Diversification: A Must for Personal Finance, Asset Allocation, and Risk Management”

Diversification is the key to risk management in your investment portfolio.

If you invest all your money in stocks and the market crashes, you could lose a lot if you need funds immediately. But if you also invest in bonds, gold, and real estate, their gains can offset your losses in such situations.

Effective asset allocation is the key to portfolio diversification. It decides how to distribute investments across asset classes. This is in line with your risk tolerance and financial goals.

Growth Investments in India: Making Intelligent Financial Decisions with Stocks, Bonds, and More

Many options for growth investments are available for retail investors in India. Each has its own risk and return profile.

Stocks: Buying shares of companies listed on the NSE or BSE.

Bonds: Government bonds or corporate bonds that provide regular interest.

Mutual Funds: These are organizations that pool money from many investors. They invest it in a professionally managed, diversified portfolio.

ETFs: Exchange-traded funds are similar to mutual funds but are traded on stock exchanges.

Real Estate: Buying property for rental income or capital appreciation.

Gold: A popular investment in India, often in the form of jewellery or gold ETFs.

Making intelligent financial decisions based on your risk tolerance is needed for investment planning. If you can’t do it, you can hire a professional financial planner. They can create a personal finance plan for you.

Future Planning: Building a Strong Retirement Savings Plan and Effective Tax Planning

Financial planning is important even if it seems far away. In India, options like EPF, PPF, and NPS offer tax benefits. They should be part of your retirement savings plan.

Maximising Tax Savings in Your Personal Finance Strategy

Tax planning is key to smart investing. It helps boost returns by reducing taxes and taking advantage of applicable tax deductions. Strategies include knowing tax brackets, using tax deductions and credits, and tax-loss harvesting.

Tax planning and knowing how your investments are taxed can help you earn more with tax savings.

Equity Investments: Long-term capital gains on equity investments are taxed at 12.5% on gains above ₹1 lakh in a year (from this year). Short-term gains are taxed at 20% (from this year).

Debt Investments: Long-term capital gains on debt funds are taxed at 20% after indexation. Short-term gains are added to your income and taxed at your income slab.

Fixed Deposits: Interest earned on FDs is fully taxable as per your income slab.

Retirement Planning with EPF, PPF, and NPS: Essential Tools for Financial Security and Independence

EPF (Employee Provident Fund): A government-backed retirement scheme for salaried employees. It’s a must for personal finance. Employees and employers contribute to the fund, and interest is earned annually. EPF is a great tool for long-term savings and has tax benefits under Section 80C.

PPF (Public Provident Fund): A popular, long-term savings scheme. It has a 15-year tenure and offers high interest rates. Under the old tax system, PPF contributions are tax-deductible under Section 80C. Interest earned is tax-free, making it a great way to build a retirement corpus.

NPS (National Pension Scheme): A government-backed pension scheme for individuals. They can contribute regularly during their working life. It invests in a mix of equity and debt. The final corpus buys an annuity for regular post-retirement income. Under the old income tax system, NPS contributions are tax-deductible under Section 80C. They also allow an extra ₹50,000 deduction under Section 80CCD(1B).

Plan for retirement

Even if this is far away, you should consider how your money will benefit your life after retirement. You have probably read a lot of advice on saving aggressively for early retirement so that every penny will continue compounding for more years. So, what is your typical retirement goal? Obviously, the rules aren’t suitable when looking at personal financial needs to find the best retirement program for the person. Details vary based on your particular situation. Can a retired person repay their mortgage before retirement? Can someone retire on his own?

Setting and Achieving Personal Financial Goals: Building a Customized Financial Plan

Personal financial planning is the first step to managing your finances. Goals can be short-term, like saving for a vacation, or long-term, like buying a home or retiring comfortably.

Steps to Set and Achieve Financial Goals

Set Your Goals: List your financial goals—short-term and long-term.

Prioritize: Rank these goals based on urgency and importance.

Action Plan: Calculate how much you need to save or invest to achieve each goal. For example, if you want to save ₹5 lakhs for a down payment on a house in 5 years, you need to save around ₹8,333 per month.

Timeline: Set deadlines for each goal.

Review and adjust: Regularly check your progress and adjust your plan as needed. If needed, you can consult financial planners for an informed decision. Life changes, and your financial plan should change accordingly.

Continuous Financial Education and Resources: Stay Informed, Stay Ahead in Personal Finance

Personal finance is complex and dynamic. It requires continuous learning, especially in India, where financial markets and tax laws change frequently. Personal finance education is essential for individuals to manage their finances effectively. Here are some resources to help you stay informed:

Books: Good starting points are books you can read to understand the basics of personal finance. Check out some suggestions in this blog.

Online Courses: Zerodha Varsity and NISM are good places to start with investing. They are the best personal finance courses online.

Financial blogs: Many good blogs offer insights into personal finance and investments, providing many free online articles for financial learning.

Conclusion: Embark on Your Personal Finance Journey Toward Financial Independence

Personal finance and investments are a continuous journey. This is true in India, where the economy, tax laws, and financial products are unique. As you grow and your finances change, so will your goals and strategies.

We must prioritize financial education. Most of us lack any formal training, so we have to rely on self-education or our parents to manage our money.

Next Steps:

Kickstart Your Personal Financial Management with a Solid Budget: Create a simple budget to track your income and manage expenses. Use the best tool according to your needs. Personal financial management is important and requires planning and discipline. You must separate your emotions from financial decisions.

Build an Emergency Fund for Essential Financial Protection and Security: Establishing an emergency fund as a financial safety net is crucial. This fund should ideally cover 3 to 6 months of living expenses, ensuring that you can manage unforeseen events without jeopardizing your long-term financial goals. By automating contributions to this fund, you ensure steady progress toward building this essential financial buffer.

Begin Your Journey in Personal Investments for Sustainable Financial Growth: Begin with a small and diversified portfolio. Increase your investments as you learn and reap the power of compounding.

Commit to Ongoing Financial Education and Literacy for Continuous Success: Stay updated on India’s latest financial trends and tax laws.

A year ago, I embarked on a transformative journey to achieve financial literacy and establish personal financial goals. This journey has not only helped me become financially stable but also significantly increased my net worth. It has been an empowering experience that has enabled me to make decisively smart personal finance decisions. Through the rigorous implementation of a strict budget, strategic investments in a diversified portfolio, and adept utilization of tax-saving instruments, I have successfully achieved many of my financial goals.

I will continue to share my journey and experiences with my friends and readers. Stay informed. Adjust as needed. Keep going. With time, discipline, and knowledge of the Indian financial system, you will be financially free.

Respected sir, very well articulated article. Please write on office politics/office bullying and how to overcome it.

Thank you. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

Very comprehensive approach to financial planning and the need to regulate one’s finanaces

Thank you. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

Had a glance over the article. Really necessary for young professionals. More impressed with the fact that dear Vishal ventured to enter into this field, totally unconnected with his present assignment. But in my opinion, financial planning is the topic, a must for everyone. My personal view is that we should teach money to each and every child even before it’s teenage starts. Every child must know the value of money; and more so that it takes hard work to earn even a little of it. Children must know how much pain their father has (parents in the present day environment) to arrange everything they desire and get.

So, Kudos to dear Vishal for this venture and my best wishes.👍👍👍

Thank you so much for your kind words and wishes 🙏

Worth reading the article

Keep up the good work

Good luck and Best Wishes to Vishal Ji

Thank you 🙏

I went through this with the critical eye of a senior retired bank executive. Sometimes, I doubted whether this article was written by a chemical engineer and senior IAS officer or by an experienced senior bank executive. I know the father of the author of this article, who was also a seasoned and experienced senior banker, and sometimes it made me doubt whether this article was co-authored by Mr. S.N. Sharma, the father of Mr. Vishal Sharma, the author of this article.

Moreover, it is one of the best articles on this topic I have ever read. My rating is 5/5. However, my advice to the author is to please also publish a shorter version of this article for the benefit of the impatient young generation of real ages. Best of luck!

Thank you for your blessings, Uncle Jee 🙏,

Coming from an experienced career banker like you means a lot to me.

Please read ” reel ages” instead of ‘real ages ‘.

That’s phenomenal writing sir. Loved the way things have been explained.

Thank you. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

Very Informative and useful

Thank you. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

extremely informative

Thank you, Harsh. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

This article is a true gem! Your personal experiences bring a unique and relatable perspective to the often complex world of finance. You’ve managed to make the topic not only understandable but genuinely engaging. It’s clear that your insights are hard-earned and valuable, making this a must-read for anyone looking to navigate their financial journey. Thank you for sharing your story—it’s truly made this piece stand out!

Thank you, Upendra. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:

https://www.hillyreviews.com/contact/

I’ve only made it halfway through this post, but I have to pause and thank you for such insightful content! Your experience in personal finance clearly shines through, and I’m already picking up gems that are going to save me a lot more than just pennies. If only managing my money was as easy as reading this blog—I’d be retired by now! Kudos to you for making wealth management sound not just achievable, but downright enjoyable.

Thank you, Suprabhat. I am glad that you can find some value in the post. Don’t forget to subscribe to the newsletter for such updates at:-

https://www.hillyreviews.com/contact/

Nicely penned. I was unaware of Vishal’s this quality. Appreciable.

You did a great job explaining key tenets of personal financial planning and offered good tools/resources. Very well done.👏

I am glad you enjoyed it 🙏

Ideas related to managements are really appreciated

Thanks !

Kudos to the idea benifical for the people of all ages. As one learns money managment he learns respecting the very hardwork one does.

Thank you, absolutely!

Explained in such a layman manner, article like this should reach every youth.

I am glad you enjoyed it 🙏

Really helpful for people new to management

Thanks Nishant 🙂

Well said 👌

Thanks!

Explained briefly, very beneficial and helpful approach 👍

Thank you Pandey Jee 🙏

Absolutely beneficial

Thank you, Papa Jee 🙏